As a small business owner, you are aware of the importance of keeping your employees healthy and happy. Providing them with a comprehensive health insurance plan is one of the best ways to do so. However, with so many options available in the market, choosing the right health insurance plan for your small business can be overwhelming. In this article, we will guide you through the different types of health insurance plans available for small businesses, and help you make an informed decision that suits your needs and budget.

Hook: Did you know that providing your employees with a comprehensive health insurance plan not only boosts their morale but also makes your business more attractive to potential hires?

Introduction

According to the National Small Business Association, over 90% of small businesses consider healthcare as the most critical issue affecting their business. However, providing a health insurance plan for your employees can be expensive, and small businesses usually struggle to find affordable options. Nevertheless, providing health insurance to your employees is essential, as it helps retain valuable employees, attract new ones, and improve their productivity.

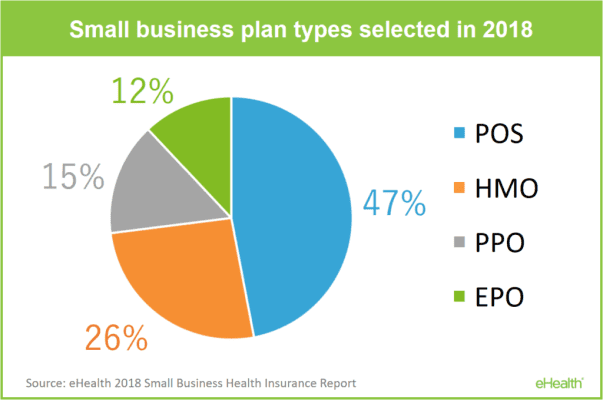

Types of Health Insurance Plans for Small Businesses

Before deciding on a health insurance plan, it is essential to understand the types of plans available for small businesses. Here are the most common types:

- Health Maintenance Organization (HMO)

- Preferred Provider Organization (PPO)

- Exclusive Provider Organization (EPO)

- Point of Service (POS)

Health Maintenance Organization (HMO)

An HMO is a type of health insurance plan that provides medical care through a network of healthcare providers. HMO plans require you to choose a primary care physician (PCP) who is responsible for coordinating all your healthcare needs. You are required to get a referral from your PCP to see a specialist, and the plan usually covers only the services provided by the healthcare providers within the network.

HMO plans are generally less expensive than other types of health insurance plans. However, they offer less flexibility in choosing healthcare providers and services outside the network.

Preferred Provider Organization (PPO)

A PPO is a type of health insurance plan that allows you to choose healthcare providers outside the network. However, using healthcare providers within the network usually costs less. PPO plans do not require you to choose a primary care physician, and you do not need a referral to see a specialist.

PPO plans are generally more expensive than HMO plans, but they offer more flexibility in choosing healthcare providers and services.

Exclusive Provider Organization (EPO)

An EPO is a type of health insurance plan that provides medical care through a network of healthcare providers. Like HMO plans, EPO plans require you to choose a primary care physician who is responsible for coordinating all your healthcare needs. However, EPO plans do not require you to get a referral to see a specialist.

EPO plans are generally less expensive than PPO plans, but they offer less flexibility in choosing healthcare providers and services.

Also check: car insurance | car insurance comparison and car insurance

Point of Service (POS)

A POS is a type of health insurance plan that combines the features of both HMO and PPO plans. Like HMO plans, you are required to choose a primary care physician who is responsible for coordinating all your healthcare needs. However, like PPO plans, you can choose healthcare providers outside the network, but using healthcare providers within the network usually costs less.

POS plans are generally more expensive than HMO plans, but less expensive than PPO plans. They offer more flexibility than HMO plans but less flexibility than PPO plans.

Factors to Consider When Choosing a Health Insurance Plan for Small Businesses

Cost

Cost is one of the most crucial factors to consider when choosing a health insurance plan for your small business. Small businesses usually have a tight budget, and it is essential to choose a plan that is affordable while still providing comprehensive coverage. Consider the monthly premiums, deductibles, co-pays, and out-of-pocket expenses of each plan before making a decision.

Network Coverage

Network coverage is another crucial factor to consider. If you have employees who travel frequently or live in different states, you may want to choose a plan with a broad network of healthcare providers. On the other hand, if most of your employees live in a particular area, a plan with a smaller network may be more cost-effective.

Coverage Options

Different health insurance plans offer different coverage options. Some plans may cover only basic medical services, while others may include dental, vision, and mental health services. Consider the specific needs of your employees when choosing a plan.

Employee Participation

Employee participation is another crucial factor to consider. While offering a health insurance plan to your employees is essential, it may not be feasible for all of them to participate. Some employees may prefer to opt-out of the plan if they already have coverage through a spouse or parent. Make sure to choose a plan that offers voluntary participation to avoid penalties for non-participation.

Conclusion

Choosing the right health insurance plan for your small business can be a daunting task. However, by understanding the different types of plans available, considering the cost, network coverage, coverage options, and employee participation, you can make an informed decision that suits your needs and budget. Remember, providing a comprehensive health insurance plan to your employees is not only beneficial for them but also for your business’s success.